It's obvious now, that the majority of the selloff has been driven by high beta nasdaq names.

Here's another way to look at it.

Below is a chart of the VIX. It measures supply and demand for S&P options:

And now a chart of VXN, which measures the supply and demand of Nasdaq options.

See the difference? The "fear" in the S&P is nowhere near the levels seen in early February, while the "fear" in the Nasdaq has gone all out of whack.

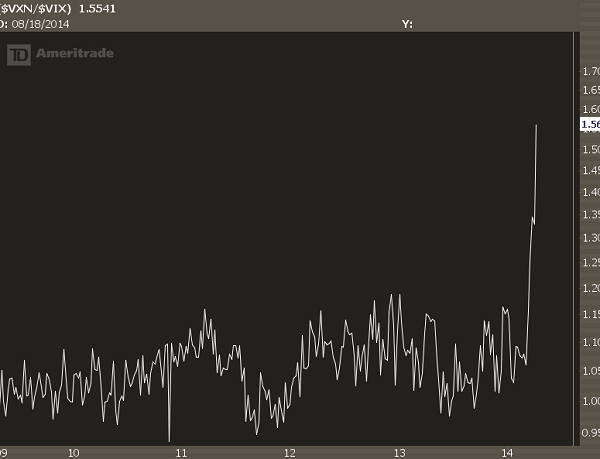

It gets even more drastic when you compare the two. Below is a chart of VXN relative to VIX, going back to 2009:

This means if you are looking to get short volatility (both actual and implied), selling options in the NDX and related options will give you a better bang for your buck.