In a "normal" market, the options market tends to have a lot of weekly option sellers, and the option buyers hang out in longer dated options.

By using the implied volatility in the options to determine this supply and demand, we can compare options that have different expiration dates.

This is the idea for "term structure."

So in a "normal" market, the implied volatility for weekly options tends to be lower than monthly options.

But when the market gets scary (for investors), this relationship will switch.

The weekly options will get more expensive (on a relative basis) compared to monthly options.

And you can make moey from it.

A long calendar spread is where you short near term options and go long next term options. It makes money if the market stays in a range, if the term structure changes, and if the implied volatility rises on the next term option.

So when the term structure flipped, I emailed this trade to IWO Premium members:

Buy to Open QQQ May1/May 87 Call calendar for 0.34

Buy to Open QQQ May1/May 84 Put calendar for 0.38

This trade is known as a "double calendar"

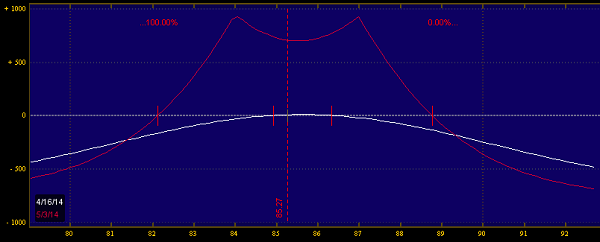

Here is what the trade originally looked like:

We were expecting the Nasdaq to "chill out" for a week or two.

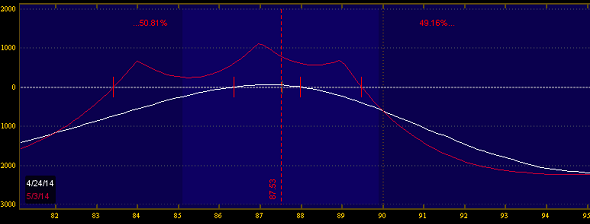

As the market squeezed higher, we added some upside protection by picking up another round of call calendars.

Buy May1/May 89 Call calendar @0.40

By doing this, we were reducing our upside risk in exchange for lower reward and more capital costs.

Here is what the trade looked like after the adjustment.

After a week of reversion, the trade ended up with a 20% return on our max risk, which is our profit target. An exit alert was sent out, explaining that you could close it out at the profit target, or try and "milk it" for additional gains.

Here was the trade at the exit alert:

Income trades like this are the bread and butter of IWO Premium. See our entire trading framework and become a member.