It seems like no matter what you do, you always end up with an iron condor that is net short.

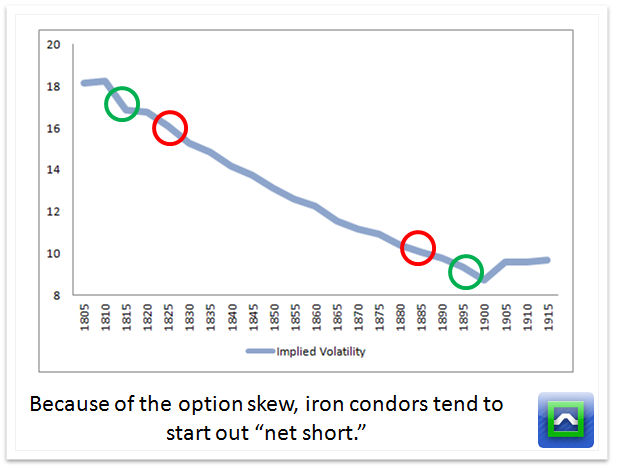

When you actually think about it, it makes sense. Because of the option skew, there will not be as much premium available on the call options and you will have to go a little closer to the current underlying price.

Do note: this applies mainly to equity options. Commodity options like gold and oil can have different volatility curves so this issue won't come up as often with those assets.

That leaves you with a little problem.

Iron condors are short vega plays, which means that if the implied volatility goes down, you can make money. But most of the time, the only way for implied volatility to head lower is if the market rallies.

And since your iron condor is net short, the directional exposure cancels out any gains from the drop in implied volatility.

It gets even worse if the market starts a grinding trend higher, which we've seen many times during the cyclical bull market that started in 2009.

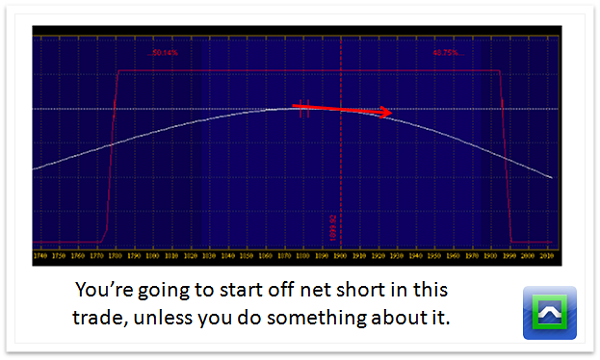

Let's take an example:

This is an iron condor with the short options at the equivalent delta-- we do this to stay consistent across different asset classes.

The max reward is 1.10, and the max risk is 3.90, which leaves us with a maximum return on risk of 28%.

But what if the market rips higher?

Since you already started off net short, you're going to be stuck at a natural disadvantage during bull markets.

How To Fix the Problem

There's a few methods to consider-- buying calls, call spreads, ratios, kite spreads, time spreads and so on.

But one simple idea has made my iron condor trading a lot more profitable.

Instead of trying to hedge using extra options on the same asset...

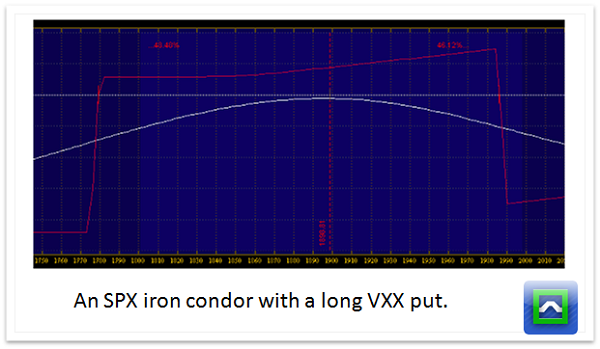

... I get short the VXX. By buying puts.

Here's the beauty of adding VXX puts to an iron condor:

Upside Risk Goes Down. Because the VXX runs with a negative correlation to stocks, getting net short VXX can give you upside hedging against the market.

Upside Ripping Risk Goes Down. If the markets have a ripper of a rally, the gamma in the long VXX puts will help to soften the blow and allow you to adjust the trade on much better terms.

It's An Extra Short Vol Trade. The VXX gets short VX futures, so it piles on your short implied volatility risk. And if the market sells off you will make money on the iron condor and lose on the VXX puts, so they help to hedge each other off.

It Makes Money Through Contango. A normal volatility curve leads to the continued grind lower in the VXX, so you can actually catch some outperformance if the market stays quiet.

The tradeoff with this is that you do lose out on higher profit potential simply because you are buying a put to hedge. The best solution to that is to pick a point in time where you are willing to take off the VXX put hedge and get a little more aggressive to the short side.

Again-- this idea works well for equity indexes like RUT, SPX, and NDX but not so much with commodity indexes because they don't track the same thing.

Want to get more returns without having to time the market? Check out my iron condor training course to get an edge in the options market.