Welcome to the shakeout.

Welcome to the shakeout.

The investor zeitgeist is currently obsessed with two things:

- High yield debt

- Fed raising rates

The outcome of the Fed is what we would call a "known unknown."

If you have some magical crystal ball that will tell you exactly what the fed will do and how the market will react to it...

... you probably paid too much for it.

We don't know how the market is going to react to the Fed. The consensus is that Rate Hike = Bad and No Hike = Good-- but how many times have we seen the reaction to the Fed meeting be one giant stop-run, fade and reversal?

Instead of trying to predict where stocks are headed, how about we focus on the volatility markets.

The Current Readings

Equity volatility is being pumped up as the Fed outcome is being treated as an earnings-like outcome for the markets.

At the time of this writing, VXST (short term volatility) is at 28% and the VIX is at 24%.

Contrast that with the actual volatility in the market which is sitting at 15%.

That's a pretty hefty premium.

My End of Year Volatility Predictions

Volatility will spike but only for a day or so. After that, the actual volatility in the market will head back to 10% or so.

Remember, after the fed meeting we've got a week then Christmas. Overall trade and liquidity will wind down as trade books close and fund managers wrap up their

As the main risk event investors are concerned about is the Fed, the need for post-Fed protection will be less. The holiday trading season will get priced in and we'll see the VIX head lower. January SPX options and VIX futures will also see their premium levels drop.

If anyone buys protection it's going to be out in February. That will coincide with the start of earnings season for stocks. On top of that, the next Fed meeting will be at the end of January, which is after options expiration.

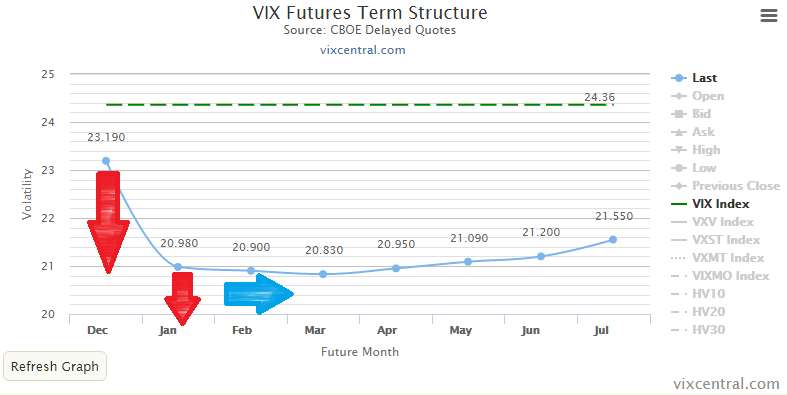

Looking at the VIX futures curve, here's what I expect:

Technically, December VIX futures expire before the Fed meeting but the overall idea here is that:

- Near term vol goes down

- Jan vol goes down

- Feb vol probably heads lower but stays bid relative to jan

- VIX futures curve will head back into contango

What If I'm Wrong

My opinion is that the current premiums being traded in stock options is very rich and will not be justified.

And remember...

the only way for it to be justified is if we actually see a larger volatility move than what the market is pricing in.

As an example, the SPX Dec options chain is pricing in about 50 handles worth of movement.

If you think we can move bigger, then you should be buying the straddles right now.

It's possible that this trade thesis doesn't pan out.

I believe that the only way I'm wrong is if we see a non-fed catalyst come out.

It would have to do something with the high yield debt risk spilling over, or potentially a large oil firm that surprises with ugly guidance.

Maybe something out of a BRIC nation. But none of those catalysts are really expected until the beginning of the new year.

How to Position Into It

I've already structured trades into this trade thesis, let's have a look at a few:

Sell Put Spreads In Relative Strength Names. It's easier to hunt for a bottom in stocks like FB and AMZN than it is in the S&P 500. Good stock selection has worked great in 2015 and I expect it to continue into the end of the year.

Shorting VXX. I'm not going crazy short here, but I do have some smart limited risk plays that profit if VXX starts to trade lower.

Income Trades in Jan and Feb. Take advantage of the high option premiums and the holiday trading season by deploying iron condors, butterflies, and calendars. Don't overstay your welcome and look to scale in if we do end up seeing a big move.